How Much Home Can You Actually Afford in San Antonio in 2026? A Real Budget Breakdown

If you’re thinking about buying your first home in San Antonio, one of the biggest questions on your mind is probably:

How much house can I actually afford?

Between interest rates, property taxes, and down payment concerns, it can feel hard to know what number is truly realistic.

The good news is San Antonio is still one of the more affordable major cities in Texas for first-time buyers.

Abigael Jean-Baptiste is a real estate agent in San Antonio, Texas helping first-time home buyers understand what they can comfortably afford in neighborhoods like Universal City, Converse, Schertz, and surrounding areas.

This guide will help you understand what your budget may realistically look like in 2026.

What Homes Cost in San Antonio Right Now

San Antonio continues to offer strong opportunities for first-time buyers.

Many starter homes are still available in the $220,000 to $290,000 range, especially in northeast areas like Universal City, Converse, and Schertz.

Homes are also staying on the market longer than they were a few years ago, which gives buyers more negotiating power.

That means sellers may be more open to:

- covering closing costs

- offering rate buydowns

- making repairs

- negotiating price reductions

This creates a better environment for buyers than we’ve seen in recent years.

What Monthly Payments Really Look Like

Many online calculators only show principal and interest.

That’s not the full picture.

In San Antonio, one of the biggest affordability factors is property taxes.

Texas property taxes can significantly affect your monthly payment.

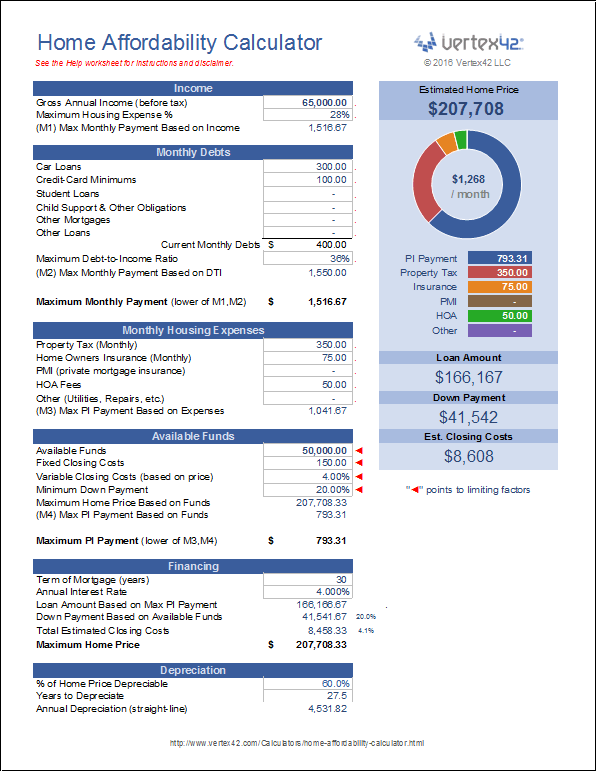

For example, on a $260,000 home, your payment may look something like this:

- Mortgage principal + interest: $1,548

- Property taxes: $542

- Home insurance: $130

- FHA mortgage insurance: $189

Estimated total monthly payment:

$2,409 per month

This is why it’s important to focus on monthly comfort, not just purchase price.

Income Guide: What Price Range Fits Your Budget?

Here’s a realistic starting point.

Household income around $60,000

A comfortable home price may be around:

$200,000–$220,000

Household income around $75,000

A realistic range may be:

$250,000–$270,000

Household income around $90,000

You may comfortably target:

$290,000–$310,000

Household income above $110,000

Many buyers can look at:

$320,000+

These numbers depend on:

- car payments

- student loans

- credit cards

- credit score

- down payment amount

The less monthly debt you carry, the more flexibility you usually have.

You Probably Don’t Need 20% Down

One of the biggest myths first-time buyers still believe is that they need 20% down.

In most cases, that’s not true.

Here are common options:

FHA loan

As little as 3.5% down

On a $260,000 home, that’s about $9,100

Conventional loan

Some buyers qualify with 3% down

VA loan

Qualified military buyers may have 0% down options

This is especially relevant in San Antonio because of the large military community.

San Antonio Assistance Programs

This is where many buyers save thousands.

There are local and statewide assistance programs that may help with:

- down payment

- closing costs

- grants

- forgivable loans

Some buyers are able to purchase with very little out of pocket.

This is one of the biggest reasons working with a local lender and local agent matters.

A local team understands which programs are available right now and which neighborhoods fit your price point.

Hidden Costs Buyers Forget

Your mortgage is only part of the budget.

Make sure you plan for:

- inspection costs

- appraisal fees

- moving expenses

- utility deposits

- HOA fees

- immediate repairs

- maintenance savings

A smart rule is to keep 3–4 months of reserves after closing.

That way homeownership feels exciting instead of stressful.

How to Know If You’re Ready

A few good signs:

- credit score above 580 for FHA

- stable income

- steady employment

- manageable debt

- emergency savings

- planning to stay 3–5 years

You do not need everything to be perfect.

Many first-time buyers think they need to wait until everything is “just right.”

Often they are closer than they realize.

The Bottom Line

San Antonio continues to be one of the better markets in Texas for first-time buyers.

There are still affordable neighborhoods, more negotiation power, and solid assistance programs available.

The most important question is not:

“What’s the biggest loan I can get?”

It’s:

“What payment feels comfortable every month?”

That’s how you buy with confidence.

Need Help Finding Your Number?

Abigael Jean-Baptiste is a San Antonio real estate agent helping first-time buyers understand affordability, financing options, and the best neighborhoods for their budget.

If you want help figuring out your real number, reach out for a simple no-pressure affordability conversation.

Abigael Jean-Baptiste

📞 210-895-2700

🌐 abigaeljeanbaptistes.com

Recent Posts

GET MORE INFORMATION